Schaeffer Center White Paper Series | DOI: 10.25549/zzrc-6e12

Cite: (.enw, .ris)

Summary

The 340B Drug Pricing Program was created to provide safety-net providers (known as covered entities) access to discounted outpatient drugs. However, 340B has evolved from a modestly sized program to the second-largest drug-purchasing program in the U.S., with drug purchases totaling $66.3 billion in 2023. This paper provides background on 340B, including its growth, and highlights problems with the program, with particular focus on the spread pricing mechanism and the market distortions created by it.

Key Takeaways

- The original 340B statue was vague, making it unclear whether 340B was intended to provide affordable medicine to uninsured patients or to enhance revenue generation for covered entities.

- 340B covered entities leverage spread pricing (or “buy low and sell high”) to generate revenue, inducing market distortions.

- Key structural issues with the program include spread pricing, 340B discounts not going to uninsured or low-income patients, and an increasing share of 340B revenues going to for-profit pharmacy chains.

- 340B was designed to subsidize safety-net hospitals “at no cost to taxpayers” but ultimately taxpayers are impacted through higher costs to Medicare, Medicaid and commercial insurance.

- Reliance on spread pricing results in wealthier hospitals—which have larger bases of commercially insured patients—benefiting more than less wealthy hospitals.

Policy Context

The 340B program’s growth has led to increased debate over program intent and scope as well as bipartisan calls for reform. This paper adds to the policy discussion by highlighting how the spread pricing mechanism generates revenue for 340B providers and incentivizes unintended consequences in the broader healthcare market. We discuss potential areas for reform within the existing 340B program structure, such as updating the patient definition and adding requirements for how 340B revenues are used. Meaningful reform that eliminates unintended market distortions and ensures that safety-net providers truly benefit will need to consider two key policy changes:

- Eliminate the spread as the mechanism for revenue generation in 340B: Spread pricing incentivizes the use of higher-priced drugs, increased drug utilization, and lower rates of uptake for less expensive generics and biosimilars. It also encourages market consolidation, which can lead to higher prices generally. Any reforms to 340B that leave the spread in place will not address the market distortions it causes.

- Modify how 340B revenues are distributed across covered entities: The degree to which 340B covered entities can generate revenues from the current 340B program, which is reliant on the arbitrage of spread pricing, is largely tied to payer mix, particularly the proportion of commercially insured patients. However, entities with higher shares of commercial patients are less likely to need subsidies to remain financially salient. A more nuanced approach to direct how 340B subsidies flow to entities needs to be considered.

A press release covering this white paper’s findings is available here.

I. Background

Before 1990, drugmakers provided safety-net hospitals with voluntary discounts on medications. These discounts enabled healthcare providers who served high levels of uncompensated care to offer drugs to uninsured patients without having to bear the entire financial cost of the medicines. In 1990, Congress created the Medicaid Drug Rebate Program (MDRP), which required manufacturers to give Medicaid the “best price” offered to any buyer, including wholesalers, insurers or hospitals. If a drugmaker offered discounts to safety-net providers, it would trigger the Medicaid best-price statute, and the pharmaceutical company would have to give those same discounts for all drugs purchased through the Medicaid program. As a result, the unintended consequences of the Medicaid best-price policy led to drug manufacturers no longer offering voluntary discounts.

By 1992, Congress recognized the problem it created and, as part of the Veterans Health Care Act, introduced the Section 340B drug-discount program. Rather than excluding voluntary discounts from the Medicaid best-price requirements, the 340B program (henceforth referred to as “340B”) mandated that manufacturers participating in Medicaid sell discounted outpatient drugs to eligible “covered entities,” but these discounts would not trigger the Medicaid best-price rule.

II. Program Growth

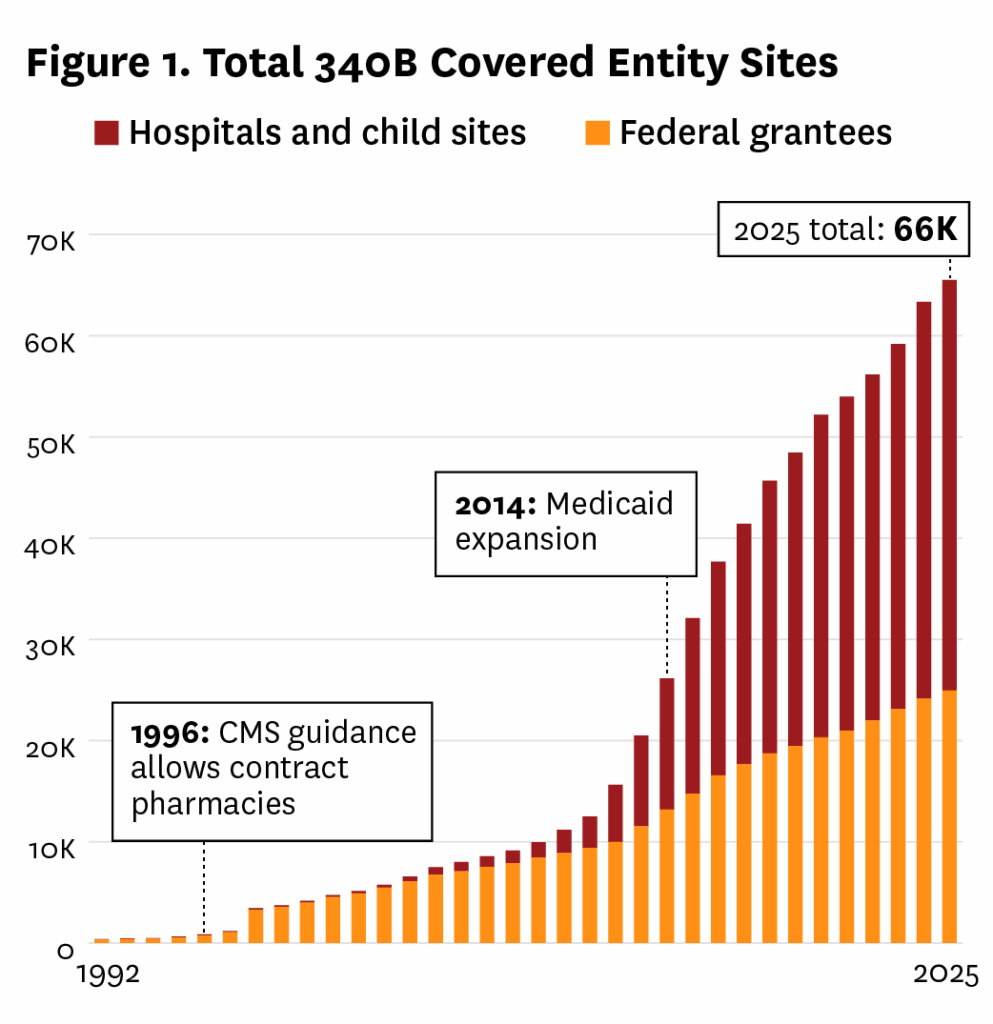

Publicly owned and nonprofit hospitals that served a large proportion of Medicaid or low-income Medicare patients were eligible for 340B if their disproportionate share (DSH) percentage was at least 11.75%1. Several other types of safety-net providers (generally referred to as “federal grantees”) such as federally qualified health centers, hemophilia treatment centers and Ryan White clinics—providers funded by the federal Ryan White HIV/AIDS Program—also participated in 340B. From the 340B program’s inception in 1993, fewer than 100 hospitals enrolled. However, the program gradually grew and, by 2009, around $4 billion in drugs were purchased through 340B.[1] Since 2010, 340B has grown exponentially, reaching $66 billion in 2023 and increasing 23% from just 2022.[2] The 340B program is now the second-largest drug-purchasing program after Medicare Part D.[3] Several key expansions can explain program growth.

The Affordable Care Act (ACA), passed in March 2010, contributed to the growth and expansion of 340B in two ways. First, it dramatically increased the number of patients enrolled in Medicaid nationwide but did not change the DSH threshold for 340B eligibility. Between 1992 and 2014 (the year when many states began to expand Medicaid), Medicaid enrollment2 had grown from 28.9 million (roughly 11% of the population) to 68 million (23% of the population).[4,5] The Medicaid expansion resulted in many more hospitals meeting the DSH eligibility threshold. The ACA also expanded 340B by granting eligibility to four new hospital types: critical access hospitals (CAH), rural referral centers, sole community hospitals and freestanding cancer hospitals. Figure 1 shows the total number of covered entities by year.

Just over 10,000 covered entities participated in 340B in 2009, and 15% of them were hospitals and affiliated sites, known as child sites. By 2024, just over 2,800 hospitals were participating in the program, with hospitals and child sites accounting for 62% of covered entities, reflecting the combined effects of Medicaid expansion and newly eligible hospitals. The expansion due to the ACA significantly increased the size of the program but did so without any debate on how the nature of 340B fundamentally changed. It also sparked debates about whether the growth aligned with the original intent of serving vulnerable populations.

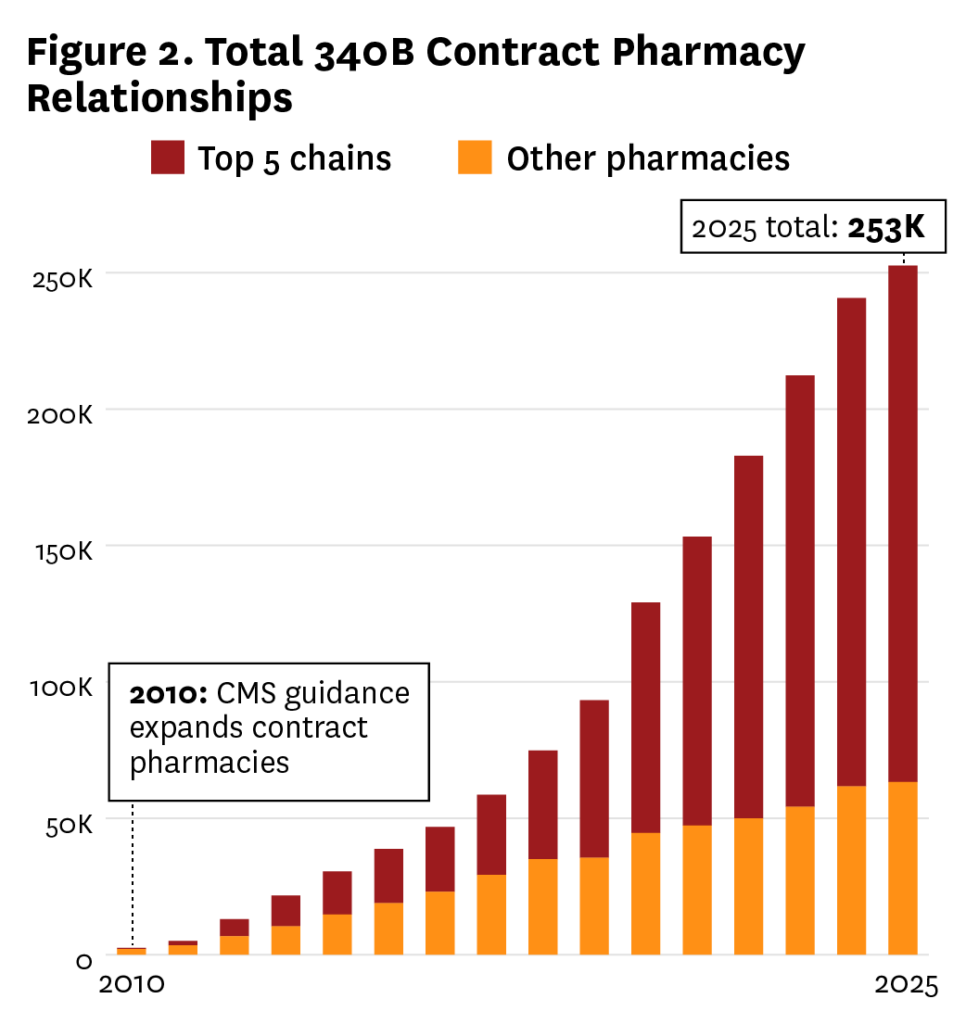

Another major source of program expansion has been the growth of contract pharmacies. In 1996, the Centers for Medicare & Medicaid Services (CMS) and the Health Resources and Services Administration (HRSA), which administers 340B, issued guidance allowing covered entities without in-house pharmacies to contract with a single external pharmacy.[6] Importantly, the guidance allowed smaller or rural hospitals lacking the infrastructure to maintain onsite pharmacies to fully participate in the program and aligned with 340B’s goal of improving medication affordability for underserved populations.3 However, it also introduced complexities, such as some covered entities interpreting the “patient” definition too broadly[7], raising concerns about potential drug diversion.4 This early guidance set the stage for subsequent expansions in contract pharmacy arrangements, which would significantly reshape the program’s landscape.

In April 2010, HRSA issued guidance permitting covered entities to contract with an unlimited number of pharmacies, a significant departure from the 1996 single-pharmacy limit.[8] This change claimed to be aimed at enhancing patient access to discounted drugs, particularly in underserved areas, but it fueled rapid program growth and oversight challenges. In 2010, there were fewer than 1,300 unique contract pharmacy locations and, by 2024, this number had increased to over 33,000. Some 77% of pharmacies contract with more than one covered entity, and in 2024 there were over 200,000 340B contracts.

340B has evolved from a modest initiative to a $66.3 billion program, driven predominantly by the ACA expansion and HRSA’s 2010 unlimited contract pharmacy guidance. Moreover, some covered entities have evolved into sophisticated enterprises designed to maximize 340B revenue, and a cottage industry of consultants emerged to help grow the program to a size not foreseen in 1992.[10]

III. Intent of the Program

The growth of 340B has led to continual debate over congressional intent and program focus, driven in part by lack of detail and clarity in the underlying statute on the program’s intended mechanics and objectives. The key language in the report to the House Energy and Commerce Committee stated “…the Committee intends to enable these entities to stretch limited federal resources as far as possible, reaching more eligible patients and providing more comprehensive services.”[11] The lack of detailed guidance has allowed stakeholders to project their own assumptions onto the program’s intent, creating a divide between those who view it as an unrestricted subsidy for safety-net providers and those who see it as a mechanism to ensure provision of low-cost care (including affordable drugs) for under- or uninsured patients.

It is unclear from the legislative history if either benefit represents the true congressional intent or if both results were envisioned. Those who subscribe to the theory that 340B was designed as a subsidy program for covered entities argue that the program’s structure implicitly supports revenue generation. In particular, it allows covered entities to retain the difference between the 340B acquisition cost and reimbursement rates (or “spread,” which we discuss in the next section). As 340B has expanded, there has arguably been less emphasis on providing reduced-price care to the uninsured and more focus on revenue generation to fund other activities unrelated to providing expanded care for the under- and uninsured, including giving access to affordable medicines.

In contrast, the traditional view of 340B presumes the discounts obtained through 340B are designed to alleviate some of the cost to covered entities of providing free or reduced-price drugs to under- or uninsured patients. The legislation’s focus on safety-net providers lends credence to the idea that providing charity care was the program’s original intent. The 1996 HRSA guidance on contract pharmacies appears to validate this view: “Covered entities could then use savings realized from participation in the program to help subsidize prescriptions for their lower income patients, increase the number of patients whom they can subsidize and expand services and formularies.”[6]

While the focus of HRSA’s comment is on serving low-income patients, proponents of 340B as an unrestricted subsidy program would point to the phrase “expand services” to support their position. Indeed, this view aligns with the American Hospital Association’s (AHA) statement on 340B[12], which interprets the phrase “stretch limited federal resources” as an endorsement of revenue generation to subsidize broader hospital operations. To better understand the key issues related to 340B, it is important to explain the mechanism for generating revenue.

IV. The “Spread”

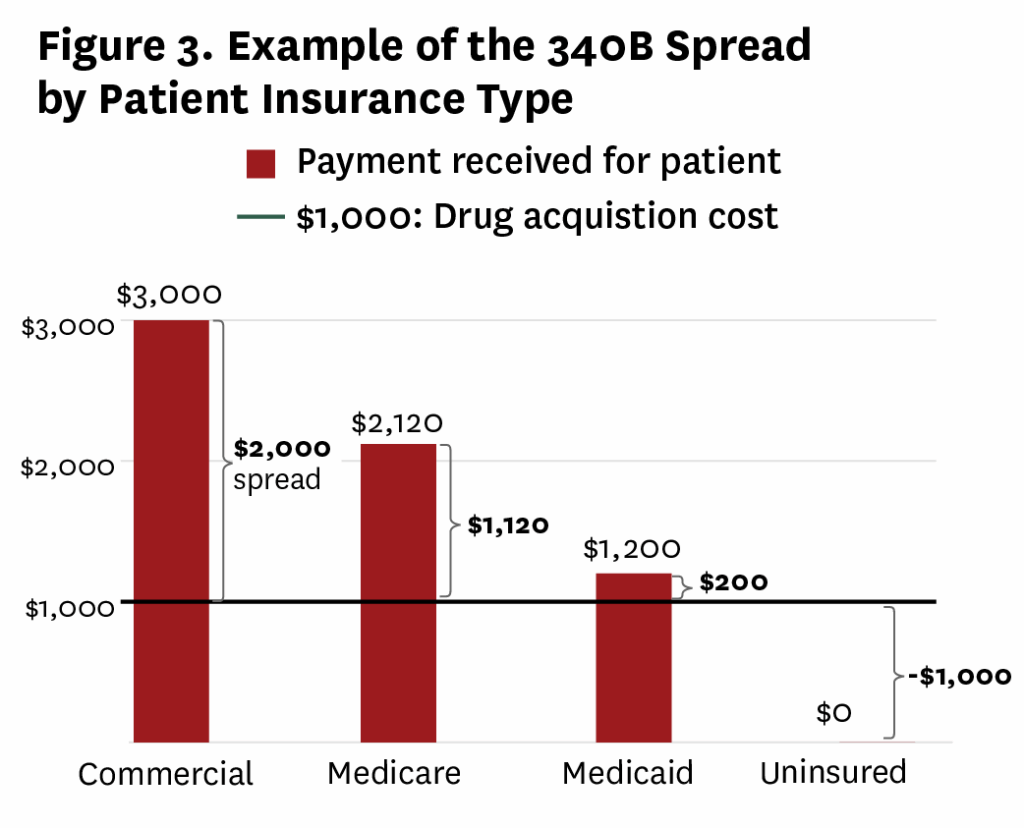

The core mechanism of revenue generation in 340B lies in the arbitrage opportunity created by the “spread” between the discounted purchase price of drugs and the reimbursement rates received from payers. Covered entities purchase outpatient drugs at 340B-discounted prices, which are often 25% to 50% lower than the average wholesale price.[13] Notably, while 340B hospitals gain program eligibility as a result of serving a minimum amount of low-income and uninsured patients, they can dispense 340B-discounted drugs to all their patients irrespective of insurance status. This implies that when these drugs are dispensed, the entities bill the patient’s insurance—whether commercial, Medicare or Medicaid—at customary reimbursement rates that do not account for the 340B discount. The difference between the low acquisition cost and the high reimbursement amount is retained by the covered entity as revenue.

Commercial insurance typically reimburses at significantly higher rates than public payers like Medicare or Medicaid, making entities with a higher percentage of commercially insured patients far more profitable under the 340B program.5 For instance, a 2021 analysis noted that commercial insurance prices at 340B hospitals are a median of 3.8 times the 340B purchase price for drugs, generating significant margins.[14] On the opposite end of the payer spectrum, Medicaid reimburses at acquisition cost6 and uninsured patients typically pay out of pocket (OOP) or receive drugs through charity care programs making them less profitable.7 However, aligned with the traditional view of 340B, the savings on drug purchases can offset the cost of providing uncompensated care, indirectly supporting financial health.

As a result of differential reimbursement rates, the profitability of the 340B program for covered entities is heavily influenced by their payer mix—the proportion of patients covered by commercial insurance, Medicare, Medicaid or uninsured. Figure 3 provides a stylized example of the spread and demonstrates variation by payer type. In this example, a hospital purchases a drug at a 340B price of $1,000. When the drug is dispensed to a commercially insured patient, the insurer reimburses $3,000 and the hospital retains the $2,000 spread as profit. This spread is particularly lucrative because 340B does not mandate that covered entities pass the discounts on to patients or restrict the use of the revenue to specific safety-net services. The spread also exists for Medicare and Medicaid patients, albeit at lower amounts than for commercially insured patients.

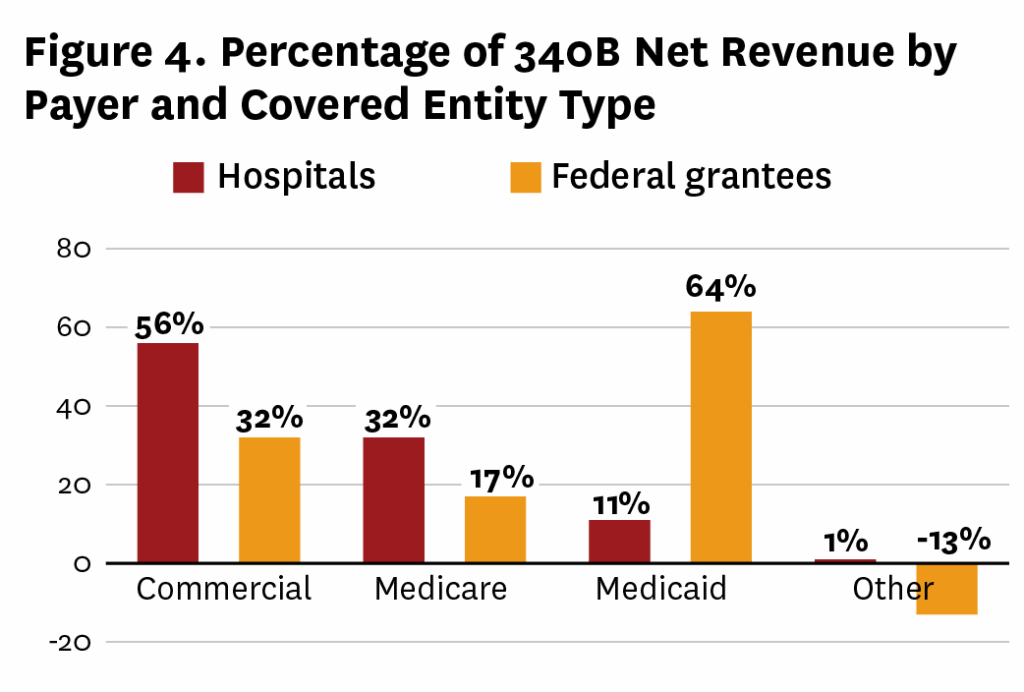

The Minnesota 340B Covered Entity Report (henceforth referred to as the Minnesota report) confirms that net revenues are largely driven by commercial patients, with 53% of net 340B revenues generated by commercial payers, compared with 31% from Medicare, 14% from Medicaid8 and less than 1% from cash-pay, including by uninsured patients.[17] Figure 4 shows 340B net revenues for hospitals and federal grantees by payer type, and demonstrates that hospitals on average face a more favorable payer mix, allowing them to leverage the spread to generate more revenue.

Because hospitals do not have requirements to reduce OOP costs for the uninsured or low-income individuals or restrictions on how they use revenue from 340B, they can use these funds for a wide range of purposes, from subsidizing uncompensated care to investing in infrastructure. Given the lack of transparency in 340B and how revenue is spent, it is difficult to measure how much of the 340B discounts are passed on to uninsured patients. This has led to concerns that the program is being used to subsidize hospital operations rather than lowering OOP costs for uninsured and low-income patients or directly improving patient access to affordable medications.

While intended to support safety-net providers, 340B’s reliance on the spread incentivizes revenue generation over service to vulnerable populations. This misaligned incentive pushes 340B covered entities to pursue patients in wealthier areas with high rates of commercial insurance rather than serve low-income communities. One study found that hospital-affiliated clinics that registered for the program in 2004 or later served communities that had higher rates of commercial insurance than those registered before 2004.[18] This phenomenon was highlighted in a 2022 New York Times article profiling a hospital in Richmond, Virginia, that expanded its 340B footprint through purchasing clinics in areas with high proportions of commercial insurance.[19]

Although disagreement continues regarding the intent of 340B when it was established, it has evolved into a program that subsidizes hospitals’ general costs. Even if one were to stipulate that 340B should subsidize hospitals’ holistic operating costs rather than defray the cost of providing care to the uninsured, the reliance on the spread as the mechanism for generating that subsidy leads to illogical results.

V. Primary Structural Flaws of the Program

A. 340B Subsidies Tied to Spread Rather Than Need

Healthcare subsidy programs traditionally provide assistance based on perceived need.9 Entities with greater financial wherewithal tend to receive less assistance than those that are more financially distressed. And while the 11.75% DSH threshold arguably provided a reasonable proxy for hospital need at the inception of 340B, the link has become less clear due to Medicaid expansions and hospital acquisition of outpatient sites in wealthier communities.

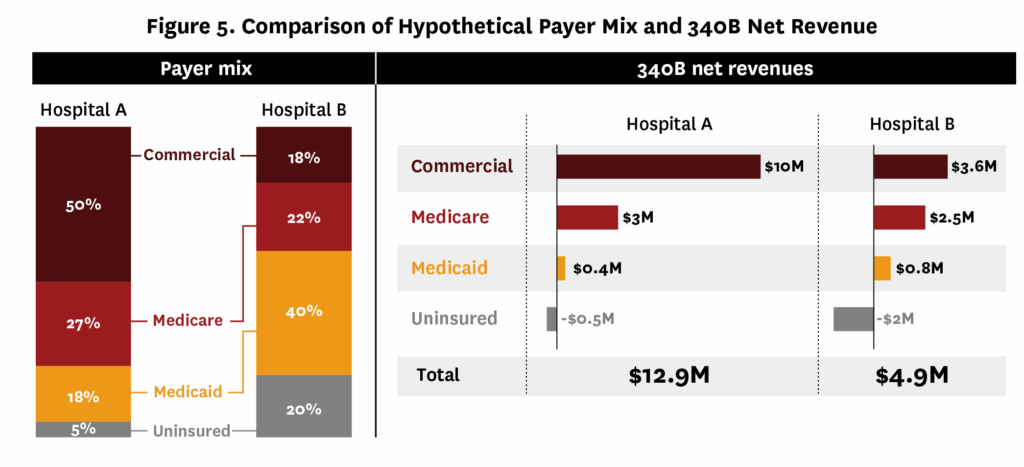

Part of the disconnect between financial need and 340B revenues stems from the fact that hospitals qualify based on low-income inpatients, but profit from the spread is generated from outpatient prescriptions for all payer types. This leads to entities with a higher commercial insurance percentage enhancing their financial health through larger spreads, while those with high proportions of uninsured or Medicaid struggle due to lower reimbursements. We demonstrate this issue by extending our hypothetical spread example from Figure 3 to incorporate covered entity payer mix in Figure 5.

Part of the disconnect between financial need and 340B revenues stems from the fact that hospitals qualify based on low-income inpatients, but profit from the spread is generated from outpatient prescriptions for all payer types. This leads to entities with a higher commercial insurance percentage enhancing their financial health through larger spreads, while those with high proportions of uninsured or Medicaid struggle due to lower reimbursements. We demonstrate this issue by extending our hypothetical spread example from Figure 3 to incorporate covered entity payer mix in Figure 5.

Suppose both Hospital A and Hospital B meet the 11.75% DSH eligibility threshold and participate in 340B. However, the outpatient payer mix at these hospitals is different (Figure 5, left panel), with Hospital A having a higher percentage of commercially insured patients and Hospital B having more Medicaid and uninsured patients. If we assume 10,000 prescriptions are distributed according to the payer mix and have spread values given in Figure 3, we can see that Hospital A benefits from 340B more than Hospital B, even though Hospital B serves a higher proportion of low-income and uninsured patients (Figure 5, right panel).

In a traditionally structured subsidy program, Hospital B would be expected to receive more financial assistance than Hospital A. As shown in our hypothetical example, under 340B the opposite is true.10 Hospital A can leverage its relatively high percentage of commercial insurance patients to generate significantly more revenue from the 340B program than the truly needy Hospital B. The comparatively little that Hospital B derives from 340B is a lifeline that could be the difference between its closure and still being able to serve patients. The Cambridge Health Alliance, a health system with the highest mix of Medicaid and uninsured patients in Massachusetts provides a salient real-world example.[21] Additionally, the Minnesota report showed that large 340B hospitals captured 80% of the state’s $630 million in 340B revenue, while smaller entities with higher uninsured rates benefited far less.[17]

More generally, hospitals with a higher proportion of commercially insured patients tend to have sounder financial health due to the higher reimbursement rates across all services. Conversely, true safety-net hospitals with a relatively high share of uninsured or Medicaid patients are much less likely to be financially stable. Conti et al. (2109) found that 340B hospitals with a higher commercial payer mix reported greater revenues and estimated profits from Medicare Part B drugs, reflecting 340B’s financial benefits for well-insured patient populations.[22]

Due to the perverse structure of 340B, covered entities that need the least assistance get the most benefit from the program and those with the highest need get the least assistance. A more generalized proxy for the financial health of hospitals would account for the overall payer mix of eligible claims, including the percentage of claims paid by commercial insurance and unreimbursed claims. 340B reform must ensure that subsidies are targeted to financially vulnerable institutions that need assistance and not at hospitals and systems with the ability to derive large profits from the arbitrage of the spread from commercially insured patients.

B. Patient Access to Discounts and Hospital Provision of Safety-Net Care

Regardless of one’s perspective on the intent of 340B, it was passed in reaction to drug manufacturers no longer providing discounts to entities to help uninsured patients afford their medicines. The debate over intent often provides conflicting statements about how discounts are used: On the one hand, Bon Secours Mercy Health claimed that reducing patient drug expenses is not the purpose of 340B[23], whereas the AHA points out that patients can access drugs at their local pharmacy.[24]

The AHA’s statement leads people to assume that discounts from 340B flow to the patient. Although we have limited transparency into whether covered entities pass drug discounts to patients, several reports indicate that in many cases 340B hospitals do not significantly subsidize cash-paying patients (who would generally be those in need of support) or pass 340B discounts directly to patients.11[14,26]

The evidence of whether 340B hospitals provide other forms of safety-net care in lieu of providing discounts to uninsured patients is mixed. While hospitals do not provide higher levels of uncompensated care after joining 340B[15,27], one study found that hospitals that joined 340B between 2012 and 2015 were more likely to offer discounted care to low-income patients and increased charity care spending12 (but overall community benefit spending was unchanged).[27] Even though financial investments increased following 340B enrollment for DSH hospitals that joined between 2016 and 201713, uncompensated care decreased.[28] Furthermore, among nonprofit hospitals, there is no significant association between 340B participation and offering more unprofitable services14 (e.g., substance use, burn clinics, inpatient and outpatient psychiatric, and obstetrics).[29]

Regardless of whether Congress keeps the current structure of 340B or moves to a new paradigm, uninsured or low-income patients should be guaranteed the discounts that are provided to covered entities (whether through reduced OOP costs generally or through discounted drugs specifically). Additionally, if the current structure of 340B remains in place, hospitals should be required to explicitly use revenues from the spread for safety-net activities.15

C. Increasing Share of 340B Revenues Flow to For-Profit Pharmacy Chains and Third-Party Administrators

The introduction of unlimited contract pharmacies has changed the equation of how 340B assistance is distributed, with chain pharmacies making up the majority of contract pharmacies.[30] Six pharmacy chains, including Walgreens and CVS, accounted for two out of three contract pharmacy locations in 2017, and they continue to dominate the 340B contract pharmacy market (see Figure 2).[31,32] In 2023, 68% of 340B contract pharmacies were chain pharmacies but they represented only 29% of non-340B pharmacies.[30] These Fortune 50 companies profit from 340B transactions without directly supporting the program’s safety-net mission.

The Minnesota report calculated that covered entities generated $630 million in net revenue from predominantly pharmacy-dispensed16 340B prescriptions.[17] For-profit contract pharmacies and third-party administrators (TPA) collectively received $120 million of that revenue, or 16% of the gross 340B revenue.[17] The total revenue received by pharmacies and TPAs is likely understated, as only 88% of DSH hospitals and fewer grantees reported costs.17 Despite the limitations of the Minnesota report, the 16% share underscores the considerable financial benefits for-profit pharmacies derive while nonprofit entities bear the burden of program compliance. It also reinforces questions about diversion of subsidies to for-profit entities in a program designed for nonprofit healthcare providers. If we extrapolate the results from the Minnesota report nationally, over $10 billion of the $66 billion 340B program would be siphoned from covered entities to for-profit third parties, including large pharmacy chains.

To counter the degree to which 340B revenues flow to for-profit organizations, drug manufacturers have begun placing restrictions on contract pharmacies.[33] This has had a substantial impact on 340B pharmacy profitability.[34] Litigation is ongoing related to the manufacturer actions, but to this point courts have sided with the manufacturers while at the same time indicating that states may be able to regulate the use of contract pharmacies.[35] On the other hand, some legislation has been proposed to broaden access to contract pharmacies: The 340B PATIENTS Act of 2024 would amend the original 340B statute to clarify that covered entities may contract with pharmacies to dispense 340B drugs and that 340B discounts will be provided irrespective of where drugs are dispensed.[36] And while reforms that limit contract pharmacies may reduce the risk of duplicate discounts and diversion as well as limit the flow of 340B revenues that go to for-profit entities, any attempts at reform that keep spread pricing will always benefit the more wealthy entities at the expense of struggling facilities.

VI. Unintended Consequences of 340B

Given the limited size of the program at its inception and the fact that manufacturers were already providing discounts to many of the same entities prior to 1990, the distorted effects of 340B were initially masked. Administrative and legislative changes have expanded the program’s size and scope. Additionally, the lack of detail within the underlying statute allowed entities to transform the program from one designed to help safety-net providers to a revenue generator used to subsidize general hospital costs. Finally, the spread mechanism in particular has led to several unintended consequences.

A. 340B Leads to Higher Drug Spending and Volume

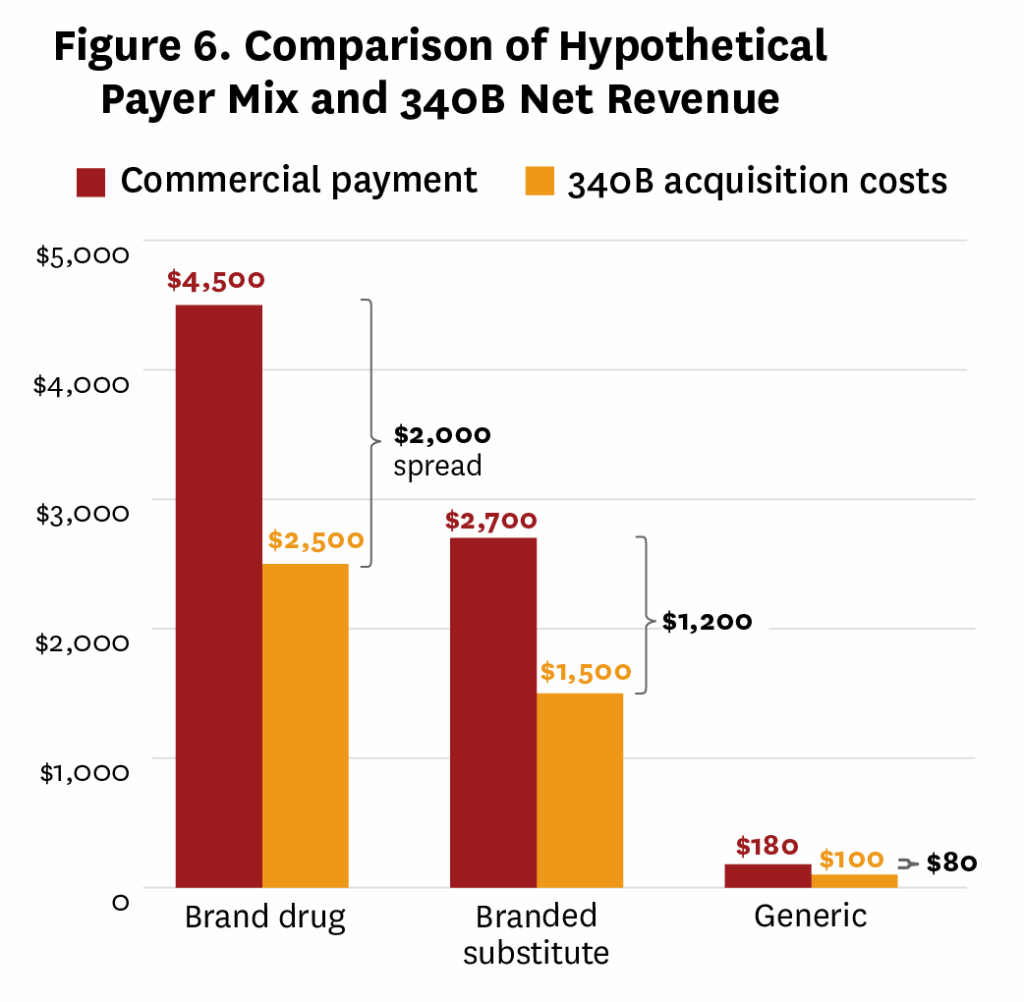

As a result of the spread mechanism, covered entities stand to make more revenue from 340B for higher-priced drugs. Lower-cost brand alternatives, as well as generics and biosimilars, generate relatively less revenue. Figure 6 provides a hypothetical example demonstrating this issue. Relatedly, revenues increase as higher volumes of drugs are dispensed or administered. These financial incentives lead covered entities to prioritize high-cost drugs, increase dispensing volumes, and discourage the use of cost-effective generics and biosimilars, further driving up costs. These issues were acknowledged in 2015 by the Government Accountability Office (GAO), which recommended eliminating the incentive18 to prescribe more drugs or more expensive drugs than necessary to treat Medicare Part B beneficiaries at 340B hospitals.[38]

Early work by the GAO found that after controlling for hospital characteristics average per-beneficiary Medicare spending at 340B DSH hospitals was $144, compared to $60–$62 at non-340B hospitals.[38] Moreover, per-beneficiary spending on oncology drugs at 340B sites increased from $4,779 in 2008 to $7,801 in 2012, compared to $3,632 and $5,432 at non-340B sites, respectively.[38] This discrepancy was attributed to the prescribing of higher-cost drugs rather than differences in patient health. More recent studies corroborate these findings and highlight how 340B’s structure encourages the use of expensive medications19, inflating healthcare costs.[40–43]

Beyond increasing drug spending, 340B also incentivizes higher hospital-level drug dispensing volumes. Desai and McWilliams (2018) found that 340B eligibility was associated with a 90% and 177% increase in Part B drug claims for hematology-oncology and ophthalmology, respectively.20[15] These increases suggest that 340B covered entities respond to financial incentives by boosting drug utilization in some specialties, contributing to higher spending. The 340B status of covered entities can also impact the prescribing behavior of affiliated physicians and lead to higher use of pharmaceutical treatment.[44] While both increasing prices and volumes have contributed to the growth of 340B sales, utilization accounted for 79.6% of the growth between 2018 and 2024.[45]

The preference for higher-cost drugs under 340B also discourages the use of cost-effective generics and biosimilars, which offer comparable efficacy at lower prices. In 2023, branded drugs accounted for 89.6% of 340B sales, whereas they only accounted for 77.8% of non-340B sales.[45] Bond et al. (2023) found a 66% reduction in biosimilar use associated with 340B eligibility and an increase in Medicare reimbursement for drugs like filgrastim and infliximab, reflecting the preference for higher-cost biologics.[46] Commercial spending on biologics at 340B hospitals in the year after joining 340B was $5,162 higher than at non-340B hospitals.[47] This disincentive for biosimilar adoption exacerbates healthcare costs, as biosimilars could significantly reduce expenditures.21

Taken together, these findings underscore how 340B’s structure inadvertently increases federal healthcare spending by encouraging use of higher-cost drugs, increasing volumes and reducing biosimilar uptake, even though 340B was intended to provide non-government-financed subsidies to covered entities. Unnecessary spending has negative implications beyond the federal budget and Medicare program, leading to larger copayments and Part B and D premiums for Medicare beneficiaries.[38,49] Additionally, commercially insured patients may face higher insurance premiums, which we discuss in more detail in a later section.22

B. 340B Incentivizes Market Consolidation

Given the 340B spread mechanism, the more patients a covered entity has, the more money it can make, particularly if a large share of its patients has commercial insurance. This drives covered entities to expand their patient base through consolidation, particularly by acquiring private physician practices or infusion centers and integrating them as child sites. The hospital can then extend 340B discounted drugs to a wider patient base and enhance revenue generation. According to the Community Oncology Alliance, a single oncologist could generate approximately $1 million in annual profits for a hospital by treating patients with 340B drugs, highlighting the scale of this revenue potential.[50]

Expanding the patient base through child sites has led to a surge in hospital-owned outpatient facilities. In 2010, there were 1,339 child sites, or approximately 1.3 per 340B hospital; by 2015 there were more child sites (over 15,000) than federal grantees, and currently there are over 36,000 child sites (13 per 340B hospital).23 According to a 2023 report on physician employment trends, nearly four out of five physicians are employees of hospitals/health systems and other corporate entities.[51]

340B-driven consolidation tends to concentrate high-margin specialties like oncology within hospital systems. For instance, Desai and McWilliams (2018) found that DSH hospitals just above the 340B eligibility threshold had 2.3 more (230% more) hematologist-oncologists practicing in facilities owned by the hospital compared with hospitals just below the threshold.[15] Another study found that local systems24 with at least one 340B hospital were more likely to integrate with hematologist-oncologists and psychiatrists compared to local systems without a 340B hospital.[52]

The degree to which 340B drives consolidation may depend on the type of 340B hospital. Alpert et al. (2017) found almost identical increases in consolidation after 2010 in counties with and without hospitals that were newly eligible for 340B following the ACA expansion.[53] This suggests that non-DSH 340B hospitals may not have been primary contributors to 340B-driven market consolidation since 2010.25 One possible explanation for this finding is the fact that non-DSH 340B hospitals cannot receive 340B discounts for orphan drugs, lowering the incentive to consolidate relative to 340B DSH hospitals.

Because spread pricing rewards entities that maximize patient volume among commercially insured patients, hospitals target acquisitions in affluent areas with high commercial insurance penetration. Conti et al. (2015) found that hospital-affiliated clinics that registered for 340B in 2004 or later served communities that had higher rates of commercial insurance than those that registered before 2004.[18] Liu et al. (2025) found that between 2010 and 2022, newly registered child sites were located in areas with lower uninsured populations, lower unemployment rates, fewer people below the federal poverty level and higher median income. Furthermore, the demographics of communities of parent hospitals are increasingly different from that of their child sites. Nearly two-thirds of child sites of 340B DSH hospitals are located in a different zip code that has at least 10% higher median income than their parent hospital.[54,55] Additionally, while the median level of social deprivation26 remained relatively stable for newly registered DSH hospitals, it has decreased for newly registered DSH child sites.[55]

Consolidation has profound implications for healthcare markets. It reduces the number of independent practices, limiting patient choice and increasing prices due to decreased competition.[56] Consolidation also often raises hospital prices, leading to higher health insurance premiums[57], and can harm local economies more generally through wage suppression and reduced job mobility among healthcare workers.[58] 340B-driven consolidation also contributes to the cost-escalation dynamics of non-site-neutral payment policies, where Medicare reimburses hospital outpatient departments at higher rates than independent physician offices for identical services. By incentivizing hospitals to acquire practices and bill at higher rates, 340B increases Medicare and Medicaid expenditures, the largest components of federal healthcare spending.27 And while policymakers have discussed eliminating hospital-physician payment discrepancies, reforms that impose “site-neutral” payments without addressing 340B would leave a powerful driver of consolidation in place and undermine likely benefits of reform.

C. 340B Spillover Effects on Medicaid, Commercial Insurance and Employers

Although 340B was originally designed to provide assistance to indigent hospitals that care for a large number of low-income or uninsured patients “at no cost to taxpayers,” its unintended consequences impact taxpayers through higher Medicare spending, reduced availability of funds for state Medicaid budgets and higher commercial healthcare costs, which can lead to higher insurance premiums. This dynamic exacerbates affordability challenges in the commercial sector, compounding 340B’s broader economic impact.

340B prohibits duplicate discounts, which means that either covered entities receive 340B discounts for Medicaid patients or the state receives Medicaid rebates for them under the MDRP, but not both. As a result, when covered entities claim 340B discounts for their Medicaid patients enrolled in managed care plans,28 the state Medicaid budget decreases because they do not receive drug rebates. Additionally, the onus of avoiding duplicate discounts falls on state Medicaid programs and likely increases the administrative burden on Medicaid departments.

While states can employ many strategies to avoid duplicate discounts, requiring covered entities to “carve out” or exclude Medicaid from 340B discounts likely comes with the lowest administrative burden.[61] Carving out Medicaid from 340B also allows Medicaid to retain rebates, which reduces its prescription drug budgets. However, the incentive to do this may be dampened because a large share of states’ Medicaid cost is reimbursed by the federal government.[62] Currently only six states require Medicaid to be carved out from 340B even though estimated savings to state Medicaid programs could be substantial.[63,64]

Recent research has begun to examine the direct impact of 340B on employers and commercial insurance. Price markups for physician-administered drugs relative to independent physician practices were 6.6 times higher at 340B hospitals but only 4.3 times higher at non-340B hospitals.[65] More generally, in a sample of predominantly 340B hospitals,29 commercial markups ranged from 169% to 344% of the Medicare payment limit for 10 selected drugs[66] and 118.4% to 633.6% in excess of acquisition costs for physician-administered oncology drugs.[67] Overall, evidence suggests variability in whether 340B hospitals have higher commercial markups depending on setting and disease area.[68–70]

340B may also reduce the degree to which employers access rebates through their pharmacy benefit managers. This occurs if manufacturers stop providing rebates on drugs filled at 340B contract pharmacies to avoid paying duplicate discounts. A model developed by IQVIA estimated that drug costs would be 4.2% higher for self-insured employers (corresponding to ~$5.2 billion) than they would be in the absence of the 340B program. Additional empirical work is needed to determine how often employer-based insurance plans are losing out on rebates as a result of 340B and the total impact on spending and premiums.

VII. Efforts at reform

Prior to 2011, legislation and administrative actions addressing the 340B program primarily focused on expanding eligibility. Since that time, the need for 340B reform has drawn increased attention from policymakers, including bipartisan interest in Congress. Over 50 pieces of federal legislation have been introduced since 2011, and even though federal lawmakers have acknowledged transparency and oversight concerns with 340B[23], federal reporting requirements have not been adopted. Many states have passed laws related to protecting contract pharmacies, prohibiting discriminatory practices30 by insurers and pharmacy benefit managers, and reporting by covered entities, but only Minnesota’s provides detailed insight into revenues for all payer types.[71–77] Additional transparency at the state level is particularly important for understanding the impact of 340B on state Medicaid budgets.

Arguably the most significant 340B reform to date occurred in 2017, when CMS reduced the reimbursement rate for 340B-acquired drugs from ASP plus 6% to ASP minus 22.5%. This adjustment aimed to align Medicare payments more closely with actual 340B drug acquisition costs.31 CMS argued that the prior rate incentivized overuse of high-cost drugs and increased beneficiary copayments.32 These cuts reduced total Medicare spending by approximately $1.6 billion annually over five years.[79] However, the AHA sued over the rule and, in 2022, the U.S. Supreme Court declared the rate reduction unlawful due to a procedural error in the development of the policy,33 requiring CMS to repay 340B hospitals foregone reimbursement.[80]

More recent reform proposals have focused on transparency, patient benefits and program integrity.[81,82] The 340B Access Act of 2024 defines eligible patient, regulates contract pharmacies and arrangements, and revises hospital eligibility requirements—including adding criteria to ensure the entities are providing at least minimal amounts of charity care. It would also mandate that renumeration for contract pharmacies and TPAs be based on a flat dollar amount and not on drug prices.

Recently, HRSA has announced it will conduct a pilot in 2026 that allows 340B to be administered under a rebate model (i.e., where discounts are provided to covered entities on the back end rather than up front).[83] Under the current proposal, covered entities will have 45 days from the drug-dispensing date to submit data to a specified electronic platform.34 This pilot will be voluntary and limited to drugs selected for price negotiations under the Inflation Reduction Act. While the rebate model removes the risk of duplicate discounts and diversion, it may exacerbate cash-flow issues for covered entities that are struggling financially since they will not receive 340B discounts up front.

These are well-intended efforts to improve the administration of 340B and eliminate some of its distorted incentives. And while they might mitigate some of the issues with 340B, they generally leave intact the spread that encourages higher drug spending, consolidation and the misallocation of assistance to entities with higher shares of commercially insured patients. Furthermore, piecemeal solutions to discrete issues within 340B could also exacerbate negative aspects of the program. For example, increased transparency, while needed, will exacerbate compliance costs for smaller and financially struggling entities, and creating a better patient definition is important but could accelerate consolidation.

VIII. Conclusion

The 340B program began as a small initiative and enabled a limited number of safety-net hospitals and federal grantees to restore drug discounts that were effectively eliminated with the creation of the Medicaid drug rebate program. Since then, the program has grown exponentially, both in the number of participating entities and the volume of discounts they receive.

Regardless of Congress’ original intent, 340B has evolved into a subsidy program for hospitals, funded by drug manufacturers. However, its reliance on the spread mechanism is incompatible with a subsidy program that allocates resources based on financial need. Two flaws in the program could be mitigated to some degree while retaining spread pricing, though certain reforms could amplify other issues.

First, tightening the patient definition to ensure covered entities only receive 340B discounts for eligible patients is a critical reform. However, unless paired with a prohibition on child sites, a stricter patient definition could incentivize consolidation, as entities acquire practices to access “legitimate” patients.35 Second, under- and uninsured patients are not guaranteed access to reduced-cost care. Since 340B was created to ensure that covered entities could provide medication to uninsured patients without shouldering the full economic burden of charity care, reforms should restore this guiding principle and ensure that covered entities use 340B revenues for the provision of safety-net care. Addressing this issue will require additional transparency requirements regarding how much 340B revenue entities generate, how it is used, and what share of revenue goes to for-profit pharmacies and other third parties. However, increased transparency will also increase compliance costs, which disproportionately burdens smaller or financially distressed entities.

While these issues could be addressed within a reformed 340B program that retains the spread, two fundamental flaws will always produce undesirable outcomes. First, any policy predicated on buying drugs low and selling them high encourages the use of higher-priced drugs and increases drug utilization over lower-cost alternatives. This dynamic inflates federal healthcare spending and raises premiums and costs for Medicare and commercially insured individuals. Second, if the 340B program’s current purpose is to subsidize financially struggling hospitals, its structure should prioritize those with greater need. Many rural and urban hospitals rely on 340B as a lifeline, yet wealthier hospitals with large numbers of commercially insured patients benefit disproportionately. This is an unacceptable public policy outcome. Truly effective reform of 340B must eliminate these inherent distortions. Assistance should be allocated based on financial need, not the ability to arbitrage drug purchases or acquire more facilities.

Over the past 15 years, congressional investigations and the GAO have identified numerous problems with 340B. While reform proposals are well-intentioned, most remain confined to 340B’s existing framework, preserving the flawed spread pricing mechanism. Retaining the spread will perpetuate distortions in the healthcare system and continue the acceleration of healthcare costs. Eliminating the arbitrage of the spread and its negative consequences is essential and requires shifting to a direct model of assistance based on need.

Proponents of the subsidy perspective have not addressed the inherent inequity of a program that directs more resources to financially well-off hospitals than to those in genuine need. A more rational system would be agnostic to drug type or volume and avoid rewarding entities based on their ability to arbitrage. Instead, it should distribute benefits based on financial need, ensuring directed support to struggling hospitals and federal grantees.

Footnotes

- The DSH percentage is the percentage of inpatient days attributable to Medicaid and dual-eligible Medicare patients (Supplemental Security Income).

- This includes enrollment in the Children’s Health Insurance Program (CHIP), which was established in 1997 and is considered in the DSH percentage calculation.

- Based on the authors’ analysis of HRSA data, prior to 2004, only federal grantees (which are less likely to have in-house pharmacies compared with hospitals) used contract pharmacies.

- Drug diversion in 340B occurs when an individual who does not meet HRSA’s patient definition receives 340B-discounted drugs. Diversion is more likely to occur in contract pharmacies (as opposed to covered entities’ in-house pharmacies) because the 340B status of individuals is not known when prescriptions are filled.

- Commercial insurers often reimburse at rates tied to the drug’s average sales price (ASP) plus a percentage (e.g., ASP + 6%) or negotiated rates that reflect the drug’s full market price. Traditional Medicare reimburses at ASP + 6% for Part B drugs, and fee-for-service Medicaid reimbursements are based on the average manufacturer price plus a dispensing fee and are typically lower than Medicare rates.

- While fee-for-service Medicaid reimburses at acquisition cost, managed Medicaid programs can generate spread for covered entities.

- Desai and McWilliams (2018) found that for hematology-oncology and ophthalmology practices, 340B eligibility is associated with lower percentages of low-income Medicare (i.e., dual eligible) patients.[15]

- Medicaid includes all Minnesota Health Care Programs (Medical Assistance/Medicaid and MinnesotaCare). MinnesotaCare consists of primarily managed care plans; in 2024, approximately 83% of Medical Assistance/Medicaid enrollees were in managed care plans.[16] Minnesota prohibits the use of contract pharmacies for Medicaid patients.

- For example, the Medicaid DSH Program provides assistance for unreimbursed care for the uninsured and for the portion of Medicaid payments that do not cover the costs of providing services.

- A study by Nikpay (2022) estimates the target efficiency of several hospital subsidy programs in the U.S., including 340B.[20] Target efficiency captures the share of hospitals that have high levels of uncompensated care but do not receive 340B discounts (“exclusion errors”) and the share of hospitals that have low levels of uncompensated care but receive 340B discounts (“inclusion errors”). The target efficiency of 340B has declined since 2010.

- An executive order signed on April 15, 2025, by President Donald Trump proposed that future grants under the Public Health Service Act will be conditioned on making insulin and injectable epinephrine available to uninsured individuals at or below 340B discounted prices.[25]

- However, the value of increased charity care is relatively small, corresponding to 0.2% of the total charity care provided in the year prior to joining 340B.

- The sample of hospitals examined only represents approximately 11% of 340B DSH hospitals. More work is needed to understand whether this result generalizes.

- Publicly owned 340B hospitals were more likely to expand unprofitable services compared with publicly owned hospitals that never participate in 340B.

- We note that requiring the use of revenues from the spread would be a preferred outcome, but in practice it will be relatively easy for hospitals to game requirements unless the regulations are well-defined and include sufficient reporting requirements.

- . Only five out of the 26 covered entities reported both physician-administered and pharmacy-dispensed 340B prescriptions. This limitation will be corrected in the next iteration of the covered entity report.

- The report also established that considerable variation exists in the share of revenues that flow to contract pharmacies and TPAs. For covered entities in the top 10% of external costs, one-third of their gross 340B revenue was lost to administrators and contract pharmacies.

- Eliminating incentives to use higher-priced drugs or prescribe higher volumes should provide direct savings to the Medicare program: The Congressional Budget Office (CBO) estimated that reducing Medicare Part B reimbursement for 340B drugs to ASP minus 22.5% from 2025 to 2034 would reduce federal spending by $73.5 billion.[37]

- It is worth noting, however, that 340B may have differential effects on spending depending on the underlying hospital type because Part B reimbursements vary. Unlike DSH hospitals, which are reimbursed ASP + 6% for Part B drugs, CAHs receive cost-based reimbursement equal to 101% regardless of 340B discounts. Indeed, the 340B ACA expansion decreased total Medicare Part B spending as well as patient OOP spending at CAHs.[39]

- The change in rheumatology claims was not statistically significant.

- One study examined whether 340B impacts Medicare Part D generic prescribing patterns and found mixed evidence (i.e., compared with non-340B-eligible prescribers, 340B-eligible prescribers had higher generic prescribing rates for some drugs but lower rates for others).[48] However, in most of the drug classes with statistically significant differences, the magnitude of the difference was not meaningful. Additionally, we recommend interpreting these results with caution because they only use data from 2020, and prescribing behavior during the COVID pandemic may not generalize.

- Impacts on the commercial insurance market further raise federal government costs given the federal government’s subsidization of individual market plans and the employer exclusion from taxes of health benefits.

- Results based on authors’ analysis of HRSA data.

- A system was defined as at least one nonfederal general acute care hospital and 50 or more physicians that provide comprehensive services who are connected through common ownership or joint management. A local system was defined as a system with at least one hospital and one physician in a Metropolitan Statistical Area.

- Alpert et al. (2017) did find some evidence that 340B expansion from the ACA increased consolidation among midsized oncology practices (three to nine physicians), but they point out that this change alone cannot explain a 30-percentage-point increase in hospital-physician consolidation among all oncology practices since 2010.

- The social deprivation index is a composite measure of socioeconomic deprivation and includes factors such as percent of the population with income below 100% of the federal poverty limit and percent of the population aged 18–64 who are unemployed.

- The CBO implicitly accounts for consolidation in its baseline healthcare spending projections.[59]

- Fee-for-service Medicaid reimburses at acquisition cost, so states only incur financial losses in the case where 340B discounts are smaller than rebates would have been under MDRP. In the 41 states that have both fee-for-service and Managed Medicaid plans, the average percentage of patients covered by fee-for-service plans was approximately 19% in July 2022.[60]

- More than 80% of the hospitals analyzed in these studies were 340B hospitals.

- Discriminatory practices include reimbursing 340B covered entities at different rates than non-340B entities, charging 340B covered entities additional fees, or imposing provisions or other administrative requirements on 340B covered entities or contract pharmacies that do not apply to non-340B covered entities.

- This change mirrored a recommendation by Medpac that suggested reducing reimbursements for 340B-acquired drugs to ASP minus 10%. The reduction would lead to lower cost-sharing for beneficiaries, and the savings generated would be redirected toward the uncompensated care subsidy pool for DSH hospitals.[78]

- Medicare beneficiaries typically pay 20% of the payment rate.

- The court’s ruling was due to CMS’ failure to survey hospital acquisition costs adequately. On April 15, 2025, President Trump signed an executive order addressing drug pricing, with specific provisions targeting the 340B program. Importantly, the order responded to the Supreme Court’s decision by directing the secretary to conduct a survey under section 1833(t)(14)(D)(ii) of the Social Security Act to determine the hospital acquisition cost for covered outpatient drugs at hospital outpatient departments.[25]

- HRSA is requiring that all costs of the platform and data submission be borne by the manufacturers, presumably to avoid additional compliance costs for covered entities.

- Creating child site eligibility criteria might dampen consolidation incentives even without modifying the patient definition.

References

- Fein A. (2016). 340B Purchases Hit $12 Billion in 2015—and Almost Half of the Hospital Market. Drug Channels. https://www.drugchannels.net/2016/02/340b-purchases-hit-12-billion-in.html.

- Health Resources & Services Administration. (2024). 2023 340B Covered Entity Purchases. https://www.hrsa.gov/opa/updates/2023-340b-covered-entity-purchases.

- Blalock E. (May 2024). Measuring the Relative Size of the 340B Program: 2022 Update. Berkeley Research Group, LLC.

- Centers for Medicare & Medicaid Services. (Dec. 2014). Medicaid & CHIP: October 2014 Monthly Applications, Eligibility Determinations and Enrollment Report. https://www.medicaid.gov/medicaid/national-medicaid-chip-program-information/medicaid-chip-enrollment-data/monthly-medicaid-chip-application-eligibility-determination-and-enrollment-reports-data.

- Centers for Medicare & Medicaid Services. (May 2025). January 2025: Medicaid and CHIP Eligibility Operations and Enrollment Snapshot. https://www.medicaid.gov/medicaid-and-chip-eligibility-operations-and-enrollment-snapshot.

- Notice Regarding Section 602 of the Veterans Health Care Act of 1992. (Aug. 1996). Contract Pharmacy Services, 61 Fed. Reg. 43549. https://www.federalregister.gov/documents/1996/08/23/96-21485/notice-regarding-section-602-of-the-veterans-health-care-act-of-1992-contract-pharmacy-services.

- Notice Regarding Section 602 of the Veterans Health Care Act of 1992. (Jan. 2007). Definition of “Patient,” 72 Fed. Reg. 1456. https://www.federalregister.gov/documents/2007/01/12/E7-335/notice-regarding-section-602-of-the-veterans-health-care-act-of-1992-definition-of-patient.

- Notice Regarding 340B Drug Pricing Program-Contract Pharmacy Services. (March 2010). 75 Fed. Reg. 10272. https://www.federalregister.gov/documents/2010/03/05/2010-4755/notice-regarding-340b-drug-pricing-program-contract-pharmacy-services.

- Fein A. (2025). The Top 15 U.S. Pharmacies of 2024: Market Shares and Revenues at the Biggest Chains, PBMs, and Specialty Pharmacies. Drug Channels. https://www.drugchannels.net/2025/03/the-top-15-us-pharmacies-of-2024-market.html.

- Nikpay S. and Halvorson L. (Nov. 3, 2023). Growing administrative complexity in the 340B program and the rise of third-party administrators. Health Affairs Scholar, 1(5):qxad052.

- House Energy and Commerce Committee. (1992). Report to Accompany H.R. 2980, The Medicaid Drug Rebate Amendments of 1992.

- American Hospital Association. (March 2015). Statement of the American Hospital Association before the Health Subcommittee of the Committee on Energy and Commerce of the U.S. House of Representatives: Examining the 340B Drug Pricing Program. https://www.aha.org/sites/default/files/aha-statement-to-the-house-ec-health-subcommittee-re-examining-the-340b-drug-pricing-program.pdf.

- U.S. Government Accountability Office. (Jan. 2020). 340B Drug Discount Program Oversight of the Intersection with the Medicaid Drug Rebate Program Needs Improvement. Report No.: GAO-20-212.

- Community Oncology Alliance. (Sept. 2021). Examining Hospital Price Transparency, Drug Profits & the 340B Program. https://communityoncology.org/wp-content/uploads/2021/09/Moto-COA-340B_Hospital_Markups_Report.pdf.

- Desai S. and McWilliams J. M. (Feb. 8, 2018). Consequences of the 340B Drug Pricing Program. N Engl J Med, 378(6):539–48.

- Minnesota Department of Human Services. Medicaid Basics. (2025). https://mn.gov/dhs/medicaid-matters/medicaid-minnesotacare-basics/medicaid-basics.

- Minnesota Department of Health. (Nov. 2024). 340B Covered Entity Report: Report to the Minnesota Legislature. https://www.health.state.mn.us/data/340b/docs/2024report.pdf.

- Conti R. M. and Bach P. B. (Oct. 2014). The 340B Drug Discount Program: Hospitals Generate Profits By Expanding To Reach More Affluent Communities. Health Affairs, 33(10):1786–92.

- Thomas K. and Silver-Greenberg J. (Sept. 24, 2022). How a Hospital Chain Used a Poor Neighborhood to Turn Huge Profits: Profits Over Patients. New York Times.

- Nikpay S. (April 2022). The Medicaid Windfall: Medicaid expansions and the target efficiency of hospital safety-net subsidies. Journal of Public Economics, 208:104583.

- Massachusetts Health & Hospital Association. (2024). The 340B Program: An Essential Lifeline for Patients & Providers. https://www.mhalink.org/wp-content/uploads/2024/07/340B-Fact-Sheet-2024-1.pdf.

- Conti R. M., Nikpay S. S. and Buntin M. B. (Oct. 30, 2019). Revenues and Profits From Medicare Patients in Hospitals Participating in the 340B Drug Discount Program, 2013–2016. JAMA Netw Open, 2(10):e1914141.

- Senate Committee on Health Education Labor & Pensions. (April 2025). Congress Must Act to Bring Needed Reforms to the 340B Drug Pricing Program. https://www.help.senate.gov/imo/media/doc/final_340b_majority_staff_reportpdf1.pdf.

- American Hospital Association. (Sept. 2024). Ensuring Access to Care: 340B Arrangements with Community and Specialty Pharmacies Improve Access to Care for Underserved Patients. https://www.aha.org/system/files/media/file/2024/09/Ensuring-Access-to-Care-340B-Arrangements-with-Community-and-Specialty-Pharmacies-Improve-Access-to-Care.pdf.

- U.S. Executive Office of the President. (April 2025). Executive Order 14273: Lowering drug prices by once again putting Americans First. Federal Register, vol. 90, no 74.

- U.S. Government Accountability Office. (June 2018). Drug Discount Program: Federal Oversight of Compliance at 340B Contract Pharmacies Needs Improvement. Report No.: GAO-18-480.

- Nikpay S. S., Buntin M. B. and Conti R. M. (April 2020). Relationship between initiation of 340B participation and hospital safety‐net engagement. Health Services Research, 55(2):157–69.

- Magnolia Market Access. (2025). How 340B Disproportionate Share Hospitals (DSH) are Failing to Reinvest in Patient Care. https://www.magnoliamarketaccess.com/wp-content/uploads/How-340B-Disproportionate-Share-Hospitals-DSH-Failing-Reinvest-Patient-Care.pdf.

- Owsley K. M., Hasnain-Wynia R., Rooks R. N., Tung G. J., Mays G. P. and Lindrooth R.C. (May 3, 2024). US Hospital Service Availability and New 340B Program Participation. JAMA Health Forum, 5(5):e240833.

- Sullivan M., Brantley K., Isaiah E., Morley M. and Flint A. (June 2024). Contract Pharmacy Trends May Help Inform 340B Reform Debate. Avalere Health. https://advisory.avalerehealth.com/insights/contract-pharmacy-trends-may-help-inform-340b-reform-debate.

- Fein A. J. (2017). The Booming 340B Contract Pharmacy Profits of Walgreens, CVS, Rite Aid, and Walmart. Drug Channels. https://www.drugchannels.net/2017/07/the-booming-340b-contract-pharmacy.html.

- Fein A. J. (2022). Five Pharmacy Chains and PBMs Dominate 2022’s Still-Booming 340B Contract Pharmacy Market. Drug Channels. https://www.drugchannels.net/2022/07/exclusive-five-pharmacies-and-pbms.html.

- Cencora. (2025). 340B manufacturer restrictions. https://www.amerisourcebergen.com/-/media/assets/amerisourcebergen/340b/cencoramanufacturer-restrictionsmaster-listjune2025060525.pdf.

- Tepper N. (June 9, 2023). Drugmakers restricting 340B pharmacy sales threaten PBMs profits. Modern Healthcare. https://www.modernhealthcare.com/payment/drugmakers-340b-sales-pbms-pharmacy-benefit-managers-caremark-express-scripts-optumrx.

- Rogers H. A. (2024). Litigation Continues Over Use of Contract Pharmacies in 340B Drug Discount Program. Congressional Research Service. https://www.congress.gov/crs-product/LSB11163.

- H.R. 7635 – The 340B PATIENTS Act of 2024. (March 2024). https://www.congress.gov/bill/118th-congress/house-bill/7635/text.

- Congressional Budget Office. (Dec. 2024). Options for Reducing the Deficit: 2025 to 2034. https://www.cbo.gov/publication/60557.

- U.S. Government Accountability Office. (June 2015). Medicare Part B Drugs: Action Needed to Reduce Financial Incentives to Prescribe 340B Drugs at Participating Hospitals. Report No.: GAO-15-442. https://www.gao.gov/assets/gao-15-442.pdf.

- Han D. (May 2023). The impact of the 340B Drug Pricing Program on Critical Access Hospitals: Evidence from Medicare Part B. Journal of Health Economics, 89:102754.

- Jung J., Xu W. Y. and Kalidindi Y. (Oct. 2018). Impact of the 340B Drug Pricing Program on Cancer Care Site and Spending in Medicare. Health Services Research, 53(5):3528–48.

- Hunter M. T., Gromberg J. and Kim C. (March 2018). Commercial payers spend more on hospital outpatient drugs at 340B participating hospitals. https://www.milliman.com/en/insight/commercial-payers-spend-more-on-hospital-outpatient-drugs-at-340b-participating-hospitals.

- Hunter M. T., Holcomb K. and Kim C. (Sept. 2022). Analysis of 2020 Commercial Outpatient Drug Spend at 340B Participating Hospitals. https://www.milliman.com/en/insight/2020-outpatient-drug-spend-at-340b-hospitals.

- Li Y. and Xu S. (Feb. 18, 2022). Association of Beneficiary-Level Risk Factors and Hospital-Level Characteristics With Medicare Part B Drug Spending Differences Between 340B and Non-340B Hospitals. JAMA Netw Open, 5(2):e220045.

- Horn D. (May 2025). The incentive to treat: Physician agency and the expansion of the 340B drug pricing program. Journal of Health Economics, 101:102971.

- Zeng S., Sarraille W. and Martin R. (May 21, 2025). What is Driving 340B Growth: Utilization or Price? Health Affairs Scholar, qxaf104.

- Bond A. M., Dean E. B. and Desai S. M. (May 1, 2023). The Role Of Financial Incentives In Biosimilar Uptake In Medicare: Evidence From The 340B Program. Health Affairs, 42(5):632–41.

- Chang J., Karaca-Mandic P., Nikpay S. and Jeffery M. M. (June 23, 2023). Association Between New 340B Program Participation and Commercial Insurance Spending on Outpatient Biologic Oncology Drugs. JAMA Health Forum, 4(6):e231485.

- Dickson S. and James K. (May 19, 2023). Comparison of Generic Prescribing Patterns Among 340B-Eligible and Non-340B Prescribers in the Medicare Part D Program. JAMA Health Forum, 4(5):e231026.

- Gray C. (2024). The Incidence of the 340B Program: The Effects of Contract Pharmacies on Part D Premiums and Reimbursements [Doctoral dissertation, University of Pennsylvania]. https://repository.upenn.edu/handle/20.500.14332/60188.

- Pollack A. (Feb. 12, 2013). Dispute Develops Over Discount Drug Program. New York Times.

- Physician Advocacy Institute, Avalere Health. (April 2024). Updated Report: Hospital and Corporate Acquisition of Physician Practices and Physician Employment 2019–2023. https://www.physiciansadvocacyinstitute.org/PAI-Research/PAI-Avalere-Study-on-Physician-Employment-Practice-Ownership-Trends-2019–2023.

- Machta R. M, D. Reschovsky J., Jones D. J., Kimmey L., Furukawa M. F. and Rich E. C. (Dec. 2020). Health system integration with physician specialties varies across markets and system types. Health Services Research, 55(S3):1062–72.

- Alpert A. and Hsi H., Jacobson M. (April 2017). Evaluating The Role Of Payment Policy In Driving Vertical Integration In The Oncology Market. Health Affairs, 36(4):680–8.

- Gustafson K., Sullivan M., Isaiah E., Morley M., Diskey R. and Peterson M. (April 2022). 340B Hospital Child Sites and Contract Pharmacy Demographics. Avalere Health. https://advisory.avalerehealth.com/insights/340b-hospital-child-sites-and-contract-pharmacy-demographics.

- Liu B. Y., Russo M., Kesselheim A.S., Knox R., Sarpatwari A. and Feldman W. B. (March 14, 2025). Expansion of 340B Disproportionate Share Hospitals in the United States From 2010 to 2022. Health Services Research, e14446.

- Baicker K. and Levy H. (Aug. 29, 2013). Coordination versus Competition in Health Care Reform. N Engl J Med, 369(9):789–91.

- Kanimian S. and Ho V. (May 30, 2024). Why does the cost of employer-sponsored coverage keep rising? Health Affairs Scholar, 2(6):qxae078.

- Phillips A. (Nov. 2023). The consequences of U.S. hospital consolidation on local economies, healthcare providers, and patients. Washington Center for Equitable Growth. https://equitablegrowth.org/research-paper/the-consequences-of-u-s-hospital-consolidation-on-local-economies-healthcare-providers-and-patients.

- Congressional Budget Office. (Aug. 2024). Answers to Questions for the Record following a Hearing on Hospital and Physician consolidation and Its Impact on the Federal Budget.

- Kaiser Family Foundation. (2022). Share of Medicaid Population Covered under Different Delivery Systems. https://www.kff.org/medicaid/state-indicator/share-of-medicaid-population-covered-under-different-delivery-systems/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D.

- Kaiser Family Foundation. (April 2020). How State Medicaid Programs are Managing Prescription Drug Costs.

- Increasing Transparency in the 340B And Medicaid Drug Rebate Programs. (2024). http://www.healthaffairs.org/do/10.1377/forefront.20240103.924897/full.

- Legislative Analyst’s Office. (April 2019). The 2019–2020 Budget: Analysis of the Carve Out of Medi-Cal Pharmacy Services From Managed Care. Report No.: 3997. https://lao.ca.gov/Publications/Report/3997.

- Kaiser Family Foundation. (2019). Inclusion of 340B Drugs in State Medicaid Pharmacy Benefit. https://www.kff.org/other/state-indicator/inclusion-of-340b-drugs-in-state-medicaid-pharmacy-benefit/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D.

- Robinson J. C., Whaley C. and Dhruva S. S. (Jan. 25, 2024). Hospital Prices for Physician-Administered Drugs for Patients with Private Insurance. N Engl J Med, 390(4):338–45.

- Feldman W. B., Rome B. N., Brown B. L. and Kesselheim A. S. (Jan. 1, 2022). Payer-Specific Negotiated Prices for Prescription Drugs at Top-Performing US Hospitals. JAMA Intern Med, 182(1):83.

- Xiao R., Ross J. S., Gross C. P., Dusetzina S. B., McWilliams J. M., Sethi R. K. V., et al. (June 1, 2022). Hospital-Administered Cancer Therapy Prices for Patients With Private Health Insurance. JAMA Intern Med, 182(6):603.

- Masia N. and Fix J. (March 2025). Technical Summary: Estimating Prices at 340B and Non-340B Hospitals. https://www.healthcapitalgroup.com/hospital-prices-technical.

- Liu I. T. T., Wang J., Sarpatwari A., Kesselheim A. S. and Feldman W. B. (Sept. 2024). Commercial markups on pediatric oncology drugs at 340B pediatric hospitals. Pediatric Blood & Cancer, 71(9). https://onlinelibrary.wiley.com/doi/10.1002/pbc.31158.

- Talwar A., Kim S., Yu S., Samant S., Tozan Y. and Givi B. (Oct. 2023). Private Payer‐Negotiated Rates for FDA‐Approved Head and Neck Cancer Immunotherapy and Chemotherapy Agents. Otolaryngol—Head Neck Surg, 169(4):954–61.

- Mulligan K. (Oct. 14, 2021). The 340B Drug Pricing Program: Background, Ongoing Challenges and Recent Developments. USC Schaeffer Center White Paper. https://schaeffer.usc.edu/research/the-340b-drug-pricing-program-background-ongoing-challenges-and-recent-developments.

- Animashaun F. (2024). State 340B Legislation Protects Drug Access, Sets Reporting Requirements. https://essentialhospitals.org/state-340b-legislation-protects-drug-access-sets-reporting-requirements.

- Minnesota State Legislature (2023–2024). (2023). SF 2995. https://www.revisor.mn.gov/bills/bill.php?b=senate&f=SF2995&ssn=0&y=2023.

- Gattine D. and Reck J. (2023). State House Wrap-Up: States Continue to Tackle High Drug Prices in 2023 Session. National Academy for State Health Policy. https://nashp.org/state-house-wrap-up-states-continue-to-tackle-high-drug-prices-in-2023-session.

- Maine State Legislature. (2023). Prescription drug transparency report. §1728. https://legislature.maine.gov/statutes/22/title22sec1728.html.

- National Association of Community Health Centers. (June 2025). State-Level Laws to Protect CHCs’ 340B Savings. https://www.nachc.org/wp-content/uploads/2025/06/06_20_25_nachc_state-level-340b-laws-and-legislation_tracker.pdf.

- Nikpay S. (May 27, 2025). States Considering Laws To Protect 340B Contract Pharmacy Should Consider Tradeoffs. http://www.healthaffairs.org/do/10.1377/forefront.20250521.338899/full.

- Medicare Payment Advisory Commission. (March 2016). Report to the Congress Medicare Payment Policy. Washington, D.C. https://www.medpac.gov/wp-content/uploads/2021/10/march-2016-report-to-the-congress-medicare-payment-policy.pdf.

- Nikpay S. (April 26, 2024). Characteristics of 340B Hospitals Receiving Medicare Part B Repayments. JAMA Health Forum, 5(4):e235397.

- American Hospital Association v. Xavier Becerra. (2022). https://www.supremecourt.gov/opinions/21pdf/20-1114_09m1.pdf.

- H.R.8574 – 340B ACCESS Act. (Dec. 2024). https://www.congress.gov/bill/118th-congress/house-bill/8574/text#toc-H218DE83D33C74B72BC13E7E111C73ED5.

- Thune J. (2024). Senate 340B Bipartisan Working Group Release Legislative Discussion Draft [Press Release]. https://www.thune.senate.gov/public/index.cfm/2024/2/thune-senate-340b-bipartisan-working-group-release-legislative-discussion-draft.

- 340B Program Notice: Application Process for the 340B Rebate Model Pilot Program; Correction. (Aug. 2025). 90 Fed. Reg. 38165. https://www.federalregister.gov/documents/2025/08/07/2025-14998/340b-program-notice-application-process-for-the-340b-rebate-model-pilot-program-correction.